387 읽음

유한양행 매출 2조 돌파, 건전성 최상이나 효율 과제

0

0

An Ample War Chest Befitting the Industry's No. 1

According to industry sources on the 3rd, Yuhan Corporation posted consolidated revenue of KRW 2.1866 trillion last year, up 5.7% from the previous year. Operating profit surged 90.9% over the same period to KRW 104.3 billion, reflecting growth in both top-line and bottom-line performance.

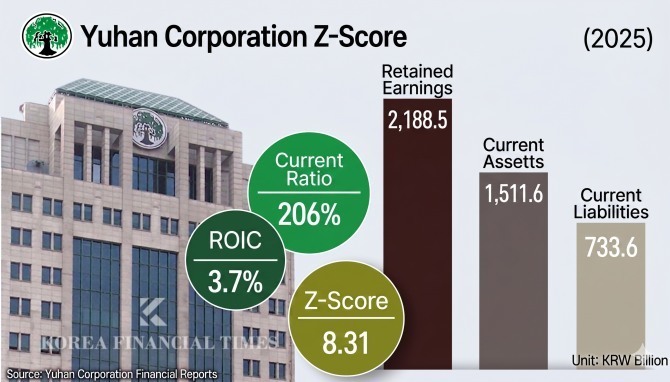

Yuhan became the first company in the industry to cross the KRW 2 trillion annual revenue threshold in 2024. Alongside this revenue growth, its financial stability indicators are also at the industry's highest level. Yuhan's Altman Z-Score stood at 8.31 in 2025, the highest among the top five pharmaceutical companies.

The Altman Z-Score is one of the metrics used by investors and financial institutions to assess a company's credit risk and to guide investment and lending decisions. A score of 3 or above is considered stable, while a score below 1.8 indicates a high likelihood of insolvency.

The foundation of this financial stability lies in the company's cash mobilization capacity and its conservative approach to debt management. As of the end of last year, Yuhan's total assets stood at KRW 3.2209 trillion, while total liabilities amounted to only KRW 858.6 billion. With a debt ratio of approximately 36.3% — far below the industry average of over 80% — Yuhan's leverage position is the most favorable among the top five pharmaceutical companies.

The gap between current liabilities — obligations due within one year — and current assets — assets convertible to cash within one year — provides an even clearer picture of Yuhan's financial strength. Last year, Yuhan's current assets totaled KRW 1.5116 trillion, more than double its current liabilities of KRW 733.6 billion.

The company's current ratio — a measure of its ability to meet short-term obligations — reached 206%, meaning it can sustain operations smoothly using its own funds without relying on external financing. In addition, retained earnings stood at KRW 2.1885 trillion, approximately twice the level of total liabilities.

Capital Efficiency Lags Behind Revenue Growth

Despite its solid financial structure, Yuhan Corporation's capital efficiency leaves something to be desired. The company's Return on Invested Capital (ROIC) was 3.7%, placing it fourth among the top five pharmaceutical companies. ROIC is a metric that measures profitability based on operating assets — in other words, it gauges how much profit is generated from the capital deployed. It is calculated by dividing Net Operating Profit After Tax (NOPAT) by Invested Capital (IC).

Yuhan's NOPAT last year was KRW 86.9 billion against Invested Capital of KRW 2.3618 trillion, yielding an ROIC of 3.7% — meaning that for every KRW 100 invested, the company earned just KRW 3.70. The return generated from deploying vast amounts of capital into its core business is essentially on par with the interest earned by depositing money in a commercial bank.

Compounding the concern over capital efficiency is a declining R&D investment ratio. Last year, Yuhan's R&D expenditures fell by KRW 26.4 billion compared to the previous year, causing the R&D spending ratio as a share of total revenue to drop from 13% to 11%. This is linked to the global rollout of Leclaza, its novel non-small cell lung cancer drug. As Leclaza entered the global commercialization track, the financial burden of costly late-stage global clinical trials eased, which is understood to have contributed to the decline in R&D spending.

A company official stated: "We are pursuing open innovation based on three strategic pillars — oncology, immunology, and metabolic diseases. Identifying investment opportunities is also part of this open innovation strategy."

Deploying Capital Into Future Growth Engines

While the easing of cost burdens is a positive development, the failure to redirect surplus capital into higher-return areas remains a challenge that must be addressed. With this sense of urgency as a backdrop, Yuhan has put forward a blueprint for its "Post-Leclaza" era and has begun the process of structural transformation.

At the center of this strategy is Targeted Protein Degradation (TPD). TPD is a platform technology that breaks down and eliminates disease-causing proteins within cells. The technology can be expanded across multiple pipelines and is capable of broadening the therapeutic scope to include previously intractable targets that conventional drugs have struggled to address.

To strengthen its capabilities in the TPD space, Yuhan established a "New Modality" division within its Central Research Institute in January and appointed Executive Vice President Jo Hak-ryeol as the division head. This move is interpreted as a signal of the company's intent to concentrate capital and capabilities on next-generation drug development.

Alongside TPD, an AI-based drug discovery platform and obesity therapeutics have also been positioned as key strategic pillars. Yuhan is leveraging its AI drug discovery platform "UNIVERSE" for candidate molecule design and screening, with the goal of unveiling a fully developed system in the first quarter of next year. The company is also co-developing a once-monthly long-acting GLP-1 obesity injectable with InventageLAB, targeting clinical entry this year.

In addition, the company has previously indicated its intention to establish "NewCo," a dedicated Research & Business Development (R&BD) subsidiary, as a means of generating revenue. Yuhan, however, clarified that the plan is "still under review."

Ultimately, the critical question will be how aggressively Yuhan can channel its accumulated capital into next-generation pipelines such as TPD and obesity treatments. Market observers are watching closely to see whether the company will be able to improve its persistently disappointing capital efficiency through capital deployment befitting the industry's top player.